Re: Bye Bye Boris!

Posted: Thu Jul 25, 2019 11:14 am

20 years ago being a DINKY (Dual Income No Kids Yet) was a signifier of affluence. Now it’s almost the minimum requirement for home ownership.Jobbo wrote: Thu Jul 25, 2019 9:46 amThey're effectively the same view. Any couple buying a house have to make an offer based on their combined earnings, because if they don't they will be outbid by someone who will. Prices are driven more by what banks are willing to lend than anything else.NotoriousREV wrote: Thu Jul 25, 2019 9:40 amView 1: affordability remains the same because most houses are bought by 2 earnersSundayjumper wrote: Thu Jul 25, 2019 9:27 am

Off the top of my head, most of the people I know have two earners in the household. I'm sure there's some data out there for regional differences.

View 2: it takes 2 wages to be able to afford a house

I think membership of the EU is incompatible with capital punishment, so we could bring that back. And we have a home secretary who supports it. This will, at a stroke, reduce overcrowding in prisons and the housing crisis (less demand because the net population increase will be slowed).NotoriousREV wrote: Thu Jul 25, 2019 11:04 am Anyone ready to put forward the case for the tangible benefits of Brexit yet? I’ll wait.

Some folk bought and got their mates in to help pay the mortgage.... in fact most people who werent in a relationship did. Modern kids want everything now with no sacrifice as said above.NotoriousREV wrote: Thu Jul 25, 2019 11:15 am20 years ago being a DINKY (Dual Income No Kids Yet) was a signifier of affluence. Now it’s almost the minimum requirement for home ownership.Jobbo wrote: Thu Jul 25, 2019 9:46 amThey're effectively the same view. Any couple buying a house have to make an offer based on their combined earnings, because if they don't they will be outbid by someone who will. Prices are driven more by what banks are willing to lend than anything else.NotoriousREV wrote: Thu Jul 25, 2019 9:40 am

View 1: affordability remains the same because most houses are bought by 2 earners

View 2: it takes 2 wages to be able to afford a house

Broccers wrote: Thu Jul 25, 2019 11:19 am Modern kids want everything now with no sacrifice as said above.

Aristotle, 4th Century BC wrote: “Young people are high-minded because they have not yet been humbled by life, nor have they experienced the force of circumstances. They think they know everything, and are always quite sure about it.”

so you’d be ok with your house value being revised to less than the mortgage you have on it?Barry wrote: Thu Jul 25, 2019 11:27 am

Bringing house values more in line with salaries would actually help me move up the ladder too, as the bigger houses would lose more based on % values of course. And that frees up cheaper houses for the new wave of buyers. Everyone wins really, if you can get over the "loss" in equity we think we have now.

I'm no economist though clearly

WHAT THE FUCK HAVE I BECOME?!!

A disappointment.JLv3.0 wrote: Thu Jul 25, 2019 11:43 amWHAT THE FUCK HAVE I BECOME?!!

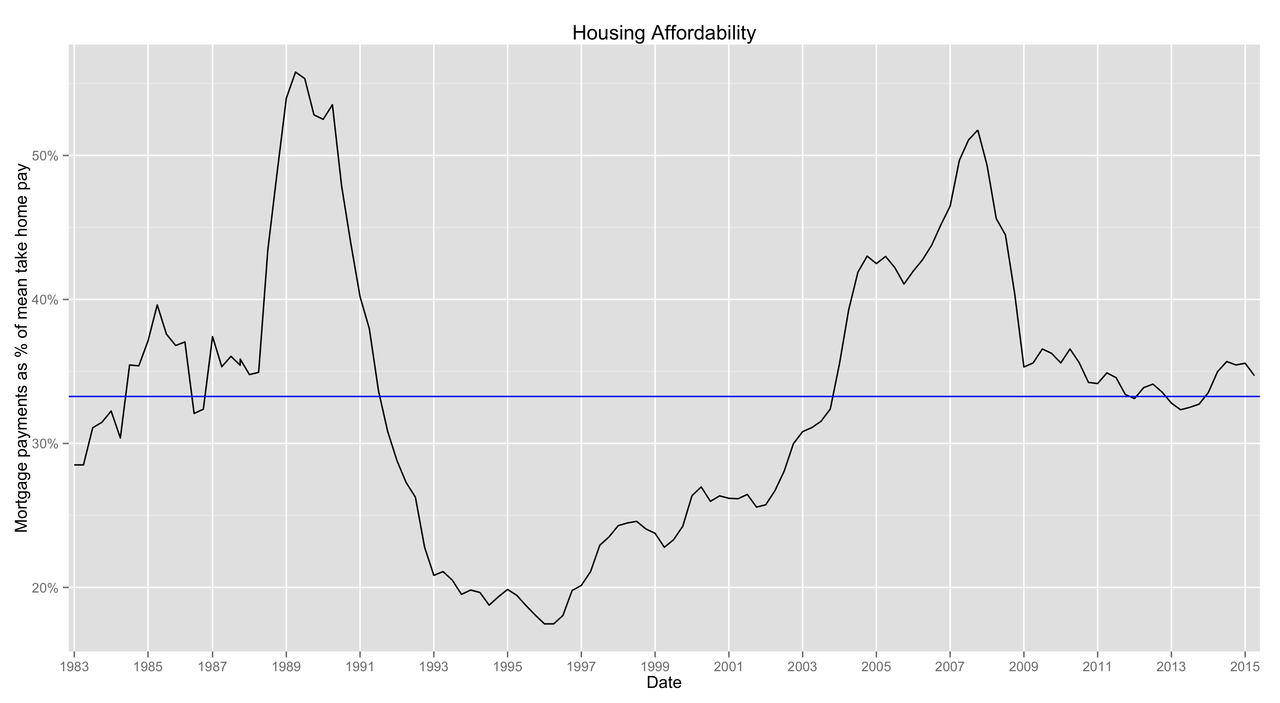

Those charts ignore deposits though. Those people that are lucky enough to be able to buy are doing so having saved up big deposits,...Jobbo wrote: Thu Jul 25, 2019 9:25 am From this Wikipedia article: https://en.wikipedia.org/wiki/Affordabi ... ed_Kingdom

The first of those is what Rev is talking about, the second is the actual monthly cost of a mortgage. I hadn't appreciated how much prices had climbed versus earnings in the last few years, though.

Exactly 20 years ago is a slightly unfair comparison, because it's quite different to 19 years or 21 years ago; the climb out of the 90s recession all seemed to happen around 1997-1999.

whilst I totally agree that deposits for first Time buyers are huge - they don’t really matter once you’re on the ladder - no one is expected to save up a 47% deposit, and you’ve presumably only got that through the increase in price of your property - which you wouldn’t have if they hadn’t gone up in price.Simon wrote: Thu Jul 25, 2019 1:17 pmThose charts ignore deposits though. Those people that are lucky enough to be able to buy are doing so having saved up big deposits,...Jobbo wrote: Thu Jul 25, 2019 9:25 am From this Wikipedia article: https://en.wikipedia.org/wiki/Affordabi ... ed_Kingdom

The first of those is what Rev is talking about, the second is the actual monthly cost of a mortgage. I hadn't appreciated how much prices had climbed versus earnings in the last few years, though.

Exactly 20 years ago is a slightly unfair comparison, because it's quite different to 19 years or 21 years ago; the climb out of the 90s recession all seemed to happen around 1997-1999.

My deposit for my current house was around 47%. No way I could afford it on my salary without that.

Of course not but that wouldn't be viable from the banks pov anyway, I'm just saying some sensible adjustment wouldn't be the worst thing. It won't happen unless the entire country crashes, I'm just making the point that you only really gain if you sell up and remove yourself from the housing chain.Rich B wrote: Thu Jul 25, 2019 11:33 amso you’d be ok with your house value being revised to less than the mortgage you have on it?Barry wrote: Thu Jul 25, 2019 11:27 am

Bringing house values more in line with salaries would actually help me move up the ladder too, as the bigger houses would lose more based on % values of course. And that frees up cheaper houses for the new wave of buyers. Everyone wins really, if you can get over the "loss" in equity we think we have now.

I'm no economist though clearly

Any sudden “sensible adjustment” would leave lots of people in negative equity - particularly first time buyers who have new mortgages and have not built up much equity....Barry wrote: Thu Jul 25, 2019 1:36 pmOf course not but that wouldn't be viable from the banks pov anyway, I'm just saying some sensible adjustment wouldn't be the worst thing. It won't happen unless the entire country crashes, I'm just making the point that you only really gain if you sell up and remove yourself from the housing chain.Rich B wrote: Thu Jul 25, 2019 11:33 amso you’d be ok with your house value being revised to less than the mortgage you have on it?Barry wrote: Thu Jul 25, 2019 11:27 am

Bringing house values more in line with salaries would actually help me move up the ladder too, as the bigger houses would lose more based on % values of course. And that frees up cheaper houses for the new wave of buyers. Everyone wins really, if you can get over the "loss" in equity we think we have now.

I'm no economist though clearly

A % adjustment would affect the expensive houses more in pure numbers than those at the lower end, is all I'm pointing out. I'm not saying it'll happen, for many reasons, and it would be financial forces causing this not intentional intervention. The current yearly increase is going to create the same result very soon anyway. I can't afford to move up significantly without agreeing to a mortgage I doubt I'd be allowed, so the situation is already there arguably.Rich B wrote: Thu Jul 25, 2019 1:40 pmAny sudden “sensible adjustment” would leave lots of people in negative equity - particularly first time buyers who have new mortgages and have not built up much equity....Barry wrote: Thu Jul 25, 2019 1:36 pmOf course not but that wouldn't be viable from the banks pov anyway, I'm just saying some sensible adjustment wouldn't be the worst thing. It won't happen unless the entire country crashes, I'm just making the point that you only really gain if you sell up and remove yourself from the housing chain.Rich B wrote: Thu Jul 25, 2019 11:33 am so you’d be ok with your house value being revised to less than the mortgage you have on it?

...which would stop them moving house for a long time. That would not help the market at all.

it really doesn’t matter what the actual numbers are, if you only own 10% of your house and the market suddenly drops by an amount more that that, you’re stuck and can’t move unless you pay the difference PLUS a new deposit. I expect there are far more people with a 10% deposit mortgage in the typical ftb market than at the top end of the market. And those at the top will likely have FAR more liquidity to absorb changes.Barry wrote: Thu Jul 25, 2019 3:58 pmA % adjustment would affect the expensive houses more in pure numbers than those at the lower end, is all I'm pointing out.Rich B wrote: Thu Jul 25, 2019 1:40 pmAny sudden “sensible adjustment” would leave lots of people in negative equity - particularly first time buyers who have new mortgages and have not built up much equity....Barry wrote: Thu Jul 25, 2019 1:36 pm

Of course not but that wouldn't be viable from the banks pov anyway, I'm just saying some sensible adjustment wouldn't be the worst thing. It won't happen unless the entire country crashes, I'm just making the point that you only really gain if you sell up and remove yourself from the housing chain.

...which would stop them moving house for a long time. That would not help the market at all.

You'd be surprised how often I've come across young couples like this in the last few years.Rich B wrote: Thu Jul 25, 2019 8:49 am If we’re generalising, twenty somethings want to buy their own houses (in the best areas), but they also want brand new German cars, annual holidays to the Far East/America/Australia, £20k weddings, £1k phones, expensive watches and clothes, new everything, etc....

If they did without all those they could probably buy a house (in a less desirable area).